In blogs like this, we sometimes like to begin discussions.

Today, we're going to present an interesting situation. Moody's holds that the US is a Aaa credit, while Apple Inc. is rated Aa1 (both its debt and its corporate family ratings are Aa1).

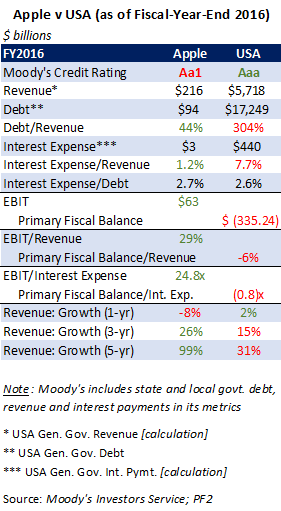

Aside from some recent hiccups, Apple is a growing company (see the chart). Its debt level sits at 44% of its annual revenues, and the expense of its debt is somewhat moderate, at 1.2% of its annual revenues. The US is growing its revenues too, albeit at a modest clip. The expense of its debt, however, is approaching 8% of annual revenues.

Recent developments make us wonder whether the US is truly the stronger credit. This blog takes you through some of the bigger picture here, including elements of the credit rating processes that might be supportive of the rating agency's stance, despite the numbers perhaps telling a different story. We don't take a position here, as much as pose the question. And we look forward to your thoughts.

Comparing Apples & Oranges? February 9th’s budget and spending caps agreement tipped next year’s budget deficit over $1 trillion, according to the Committee for a Responsible Federal Budget, despite the fact that we are almost nine years into the current economic expansion and with the official (U3) unemployment rate at just 4.1%. That bipartisan debt binge, in the wake of last year’s $1.5 trillion tax cut (over ten years), has some prudent budget-watchers scratching their heads.

Last month, Reuters reported that “China’s Dagong Global Credit Rating Co, one of the country’s most prominent ratings firms, on Tuesday cut the local and foreign currency sovereign ratings of the United States, citing an increasing reliance on debt in the world’s largest economy.” Dagong cut the US’s sovereign rating to BBB+ (from A-), with a negative outlook.

“Deficiencies in the current U.S. political ecology make it difficult for the efficient administration of the federal government, so the national economic development derails from the right track,” Dagong said. “Massive tax cuts directly reduce the federal government’s sources of debt repayment, therefore further weakens the base of government’s debt repayment.”

Looking at the numbers as of fiscal year-end 2016 (the most recent year with complete figures), Apple’s debt as a percentage of revenue and its interest expense as a percentage of revenue are much lower than the US’s corresponding levels.

Strictly based on the debt/revenue and interest expense/revenue ratios, an entity with US’s metrics would likely garner a below-investment-grade rating: according to Moody’s' ratings methodology for diversified technology companies, a negative EBIT/Interest Expense equates to a rating of Ca (the lowest rating on the subfactor scale), all else equal.

US’s Primary Balance/Interest Expense, our proxy for US’s EBIT/Interest Expense, is negative. We don’t have a proxy for the US’s EBITDA (earnings before interest, taxes, depreciation, and amortization), but let’s take our proxy for the US's EBIT and magically add back $2 trillion(!) worth of imaginary “depreciation and amortization.” Doing so gets us to an “EBITDA” of $1.7 trillion. In this hypothetical, its Debt/EBITDA is still over 10x, which would correspond to a rating of Ca (all else equal) for a diversified technology company.

Even in the rosiest possible proxy for EBITDA, in which we suppose USA has zero expenditures(!), and thus its EBITDA would simply equal its revenue, the hypothetical Debt/EBITDA would be 3x, which maps to a rating of Ba, all else equal, for a diversified technology company.

Even in the rosiest possible proxy for EBITDA, in which we suppose USA has zero expenditures(!), and thus its EBITDA would simply equal its revenue, the hypothetical Debt/EBITDA would be 3x, which maps to a rating of Ba, all else equal, for a diversified technology company.

Viewing the US’s long-term fiscal situation with a more critical lens, we might consider the future fiscal impact of Social Security and Medicare – which are underfunded by $46.7 trillion over the next 75 years (per the Fiscal Year 2016 Financial Report of the U.S. Government jointly produced by the US Treasury and the Office of Management and Budget of the Executive Office of the President).

Strictly based on the debt/revenue and interest expense/revenue ratios, an entity with US’s metrics would likely garner a below-investment-grade rating: according to Moody’s' ratings methodology for diversified technology companies, a negative EBIT/Interest Expense equates to a rating of Ca (the lowest rating on the subfactor scale), all else equal.

US’s Primary Balance/Interest Expense, our proxy for US’s EBIT/Interest Expense, is negative. We don’t have a proxy for the US’s EBITDA (earnings before interest, taxes, depreciation, and amortization), but let’s take our proxy for the US's EBIT and magically add back $2 trillion(!) worth of imaginary “depreciation and amortization.” Doing so gets us to an “EBITDA” of $1.7 trillion. In this hypothetical, its Debt/EBITDA is still over 10x, which would correspond to a rating of Ca (all else equal) for a diversified technology company.

Even in the rosiest possible proxy for EBITDA, in which we suppose USA has zero expenditures(!), and thus its EBITDA would simply equal its revenue, the hypothetical Debt/EBITDA would be 3x, which maps to a rating of Ba, all else equal, for a diversified technology company.

Even in the rosiest possible proxy for EBITDA, in which we suppose USA has zero expenditures(!), and thus its EBITDA would simply equal its revenue, the hypothetical Debt/EBITDA would be 3x, which maps to a rating of Ba, all else equal, for a diversified technology company.Viewing the US’s long-term fiscal situation with a more critical lens, we might consider the future fiscal impact of Social Security and Medicare – which are underfunded by $46.7 trillion over the next 75 years (per the Fiscal Year 2016 Financial Report of the U.S. Government jointly produced by the US Treasury and the Office of Management and Budget of the Executive Office of the President).

Yet, Moody’s and many of the other rating agencies don't seem overly concerned, rating the US Aaa (stable outlook).

Into the finer details, now, there are several quantitative factors that might be equally or more relevant to these entities’ respective ratings (e.g. EBITDA margin or FCF/Debt for Apple; Interest Expense/GDP or Inflation for the US), but we tried to highlight metrics in this chart which are most comparable between the two debt issuers.

Into the finer details, now, there are several quantitative factors that might be equally or more relevant to these entities’ respective ratings (e.g. EBITDA margin or FCF/Debt for Apple; Interest Expense/GDP or Inflation for the US), but we tried to highlight metrics in this chart which are most comparable between the two debt issuers.

Keep in mind that there are also key qualitative characteristics that Moody’s considers when rating corporates and sovereigns. For example, Moody’s gives significant weight to considerations such as management financial policy (“management and board tolerance for financial risk”) for diversified technology corporations, and institutional strength (specifically, “government effectiveness”, “rule of law”, and “control of corruption”) for sovereigns.

Notably:

- The United States government has the legal authority to compel its “customers” (i.e. taxpayers) to pay more, if necessary (although political willingness might be another matter), while a corporation has no such relationship with its customers.

- Apple lacks a printing press, whereas the USA can print its own currency.

- The US has a central bank that has the ability to monetize federal debt, whereby the Federal Reserve can essentially finance fiscal deficits by purchasing as much government debt as the federal government issues, although technically the Fed maintains its independence from political interference.

- (Moody’s does consider inflation as an important ingredient in its sovereign ratings, so the rating itself might suffer in a scenario in which the country printed its way of a fiscal hole, but there technically would still be no default.)

Altogether, Apple’s revenue is growing faster than the US’s (99% vs. 31%, over 5 years), it has much less debt than the US (relative to revenue: 44% vs. 304%), and its interest expense is much lower (relative to revenue: 1.2% vs. 7.7%).

So the question is, are the US’s other strengths or advantages -- its ability to raise more revenue through taxes if truly needed, and its unique ability to service its debts by either printing more of the world’s reserve currency or having its central bank purchase its debt -- enough to justify a Aaa rating? In deciding this, one must consider not only the US's current trillion dollar deficits at a point in the economic cycle that does not beg for drastic fiscal stimulus, but also the fact that we have a Social Security and Medicare funding gap of nearly $47 trillion, in present value terms, that is only growing worse. (At this juncture, it seems that our elected officials have chosen to do nothing about the funding gap.)

Remember, the question is not whether or not the US will default, or how it may grow itself out of the current situation -- but whether the likelihood of there being an issue here is so remote as to warrant a Aaa rating, a rating higher than that of Apple's debt, which is currently well-supported.

It is worth considering Stein’s Law as we end this blog: "If something cannot go on forever, it will stop" or "Trends that can't continue, won't." Interestingly, Stein meant this in the sense that there is no need for action or a program to make it stop, much less to make it stop immediately; it will stop of its own accord.

So the question is, are the US’s other strengths or advantages -- its ability to raise more revenue through taxes if truly needed, and its unique ability to service its debts by either printing more of the world’s reserve currency or having its central bank purchase its debt -- enough to justify a Aaa rating? In deciding this, one must consider not only the US's current trillion dollar deficits at a point in the economic cycle that does not beg for drastic fiscal stimulus, but also the fact that we have a Social Security and Medicare funding gap of nearly $47 trillion, in present value terms, that is only growing worse. (At this juncture, it seems that our elected officials have chosen to do nothing about the funding gap.)

Remember, the question is not whether or not the US will default, or how it may grow itself out of the current situation -- but whether the likelihood of there being an issue here is so remote as to warrant a Aaa rating, a rating higher than that of Apple's debt, which is currently well-supported.

It is worth considering Stein’s Law as we end this blog: "If something cannot go on forever, it will stop" or "Trends that can't continue, won't." Interestingly, Stein meant this in the sense that there is no need for action or a program to make it stop, much less to make it stop immediately; it will stop of its own accord.

|

| Lisa Benson Editorial Cartoon used with the permission of Lisa Benson, the Washington Post Writers Group and the Cartoonist Group. All rights reserved. |